Affordable Life Insurance: Protect Your Family – ssunnel

Affordable Life Insurance: Protect Your Family

In an era where financial stability is a growing concern for families, affordable life insurance emerges as a critical component of a comprehensive financial strategy. Life insurance not only provides a safety net for loved ones in the event of an untimely death but also offers a structured means of wealth transfer and savings accumulation. Understanding various types of life insurance—such as term and whole life insurance—allows consumers to make informed decisions tailored to their unique financial needs and circumstances . The implications of the Patient Protection and Affordable Care Act (ACA) emphasize the importance of equitable access to financial protections, asserting that comprehensive coverage is necessary to alleviate disparities in health and safety (Rapaport et al.), (Coronado DS et al.). Therefore, exploring affordable life insurance options becomes essential for safeguarding families against unforeseen financial burdens, ensuring a more secure future for all.

A. Importance of life insurance in family financial planning

Incorporating life insurance into family financial planning is essential for safeguarding the financial well-being of loved ones. Life insurance serves not only as a safety net for unexpected tragedies but also as a tool for long-term financial security. By ensuring that beneficiaries receive a death benefit, families can pay off debts, cover living expenses, and maintain their standard of living even in the absence of a primary income earner. This financial support can be critical during challenging times, as highlighted in the findings of the DRA Project Report No. 11-0, which emphasizes the importance of financial readiness in addressing unforeseen events (Birnbaum et al.). Additionally, the comprehensive comparison of life insurance types in illustrates the various options available, empowering families to make informed decisions about the policies that best meet their needs. Ultimately, integrating life insurance into financial planning is a proactive step toward ensuring stability and peace of mind.

II. Understanding Life Insurance

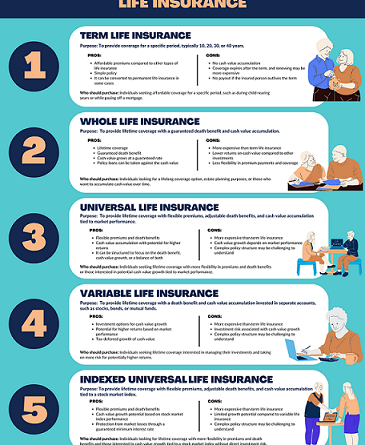

In grasping the essentials of life insurance, one must recognize its pivotal role in safeguarding the financial future of loved ones. Life insurance serves as a contract wherein the insurer guarantees a predetermined payout to beneficiaries upon the policyholders death, thus ensuring that families are not burdened by financial instability during emotionally challenging times. It is critical to evaluate the different types of life insurance available, such as term, whole, or universal life policies, each offering unique benefits tailored to specific needs and circumstances. The image that illustrates these categories, , effectively delineates the advantages and disadvantages of each type, facilitating informed decisions for prospective buyers. Moreover, addressing access to affordable life insurance requires comprehensive outreach strategies that empower individuals through education, ensuring equitable opportunities for coverage amid life transitions, as highlighted by (Ann O’Leary et al.) and (N/A). Such measures are necessary to enhance family protection through thoughtful financial planning.

A. Types of life insurance policies available

Understanding the various types of life insurance policies is essential for individuals seeking to secure financial protection for their families. The primary categories include Term Life Insurance, which provides coverage for a specified term at lower premiums, and Whole Life Insurance, offering lifelong coverage with cash value accumulation. Universal Life Insurance and Variable Life Insurance introduce greater flexibility and investment options, but they also come with increased complexity and costs. Additionally, Indexed Universal Life Insurance combines features of both universal and traditional policies, allowing for potential growth linked to stock index performance. Visual aids like can clarify these differences by succinctly illustrating the pros and cons of each option, thus empowering consumers to make informed decisions. Such knowledge is crucial as families navigate their financial futures in the context of broader socio-economic challenges outlined in (Rynell A et al.) and (Davis K), ensuring they select the most suitable policy for their needs.

| Type | Coverage Length | Builds Cash Value | Death Benefit | Best For |

| Term Life | Temporary (10-30 years) | No | Fixed | Most people, income replacement |

| Whole Life | Lifetime | Yes | Fixed | Permanent coverage, cash value growth |

| Universal Life | Lifetime | Yes | Flexible | Flexibility in premiums and coverage |

| Variable Life | Lifetime | Yes | Flexible | Investment-savvy individuals |

| Burial Insurance | Lifetime | Yes | Fixed (typically low) | Covering final expenses |

III. Benefits of Affordable Life Insurance

Affordable life insurance provides numerous benefits that are essential for ensuring the financial protection of families. Primarily, it serves as a safety net that guarantees stability in the face of unexpected events such as the loss of a breadwinner, thereby allowing families to maintain their standard of living and fulfill financial commitments without significant distress. Additionally, affordable options make life insurance accessible to a broader audience, thus promoting wider participation and awareness of financial planning. As noted in recent research, life insurance contributes not only to individual security but also to social stability and economic development (Lữ Nga P et al.). Furthermore, it often acts as a vehicle for investment, allowing policyholders to accumulate savings that can benefit their beneficiaries after their passing, enhancing the long-term financial comfort of families (Joshi KG et al.). Ultimately, affordable life insurance stands as a crucial component of family financial strategy, facilitating security and peace of mind.

A. Financial security for dependents in case of untimely death

Life insurance serves as a critical financial safety net for dependents facing the untimely death of a primary income earner. Without adequate coverage, families may struggle to maintain their standard of living, leading to substantial economic hardships. The importance of life insurance is underscored by research revealing that factors such as low income and limited awareness heavily influence policy uptake, particularly in contexts like Botswana and Malaysia, where significant portions of the population remain uninsured (Malambo et al.), (Tan et al.). Understanding the various types of life insurance, as illustrated in , can empower families to choose the optimal coverage for their unique circumstances. By investing in a suitable life insurance policy, individuals not only ensure financial protection for their dependents, but they also contribute to broader societal economic stability, thereby reinforcing the argument that affordable life insurance is an essential component of responsible family financial planning.

In summation, securing affordable life insurance emerges as a critical mechanism for safeguarding the financial future of ones family. As highlighted throughout the essay, various options such as term and whole life insurance enable individuals to tailor their coverage according to specific needs and circumstances. The decision to invest in such a policy not only serves as a protective measure but also reinforces ones commitment to family welfare, reassuring loved ones of support in times of uncertainty. As noted in discussions surrounding healthcare reforms, the intersection of financial planning and social policies can profoundly impact families’ access to critical resources, emphasizing the importance of understanding the broader implications of such decisions (N/A), (Siegel et al.). Ultimately, choosing the right insurance policy can provide peace of mind, making it essential for families to explore their options thoroughly. The insights from the comparison of life insurance types presented in further illustrate these choices effectively.

A. The necessity of choosing the right life insurance policy for family protection

Selecting the appropriate life insurance policy is a critical decision for ensuring family protection, particularly in the face of unforeseen circumstances. Families must assess their unique financial situations and future needs, which can significantly influence the effectiveness of their coverage. Different life insurance types, such as Term Life Insurance and Whole Life Insurance, come with varying benefits tailored to different family dynamics, as outlined in the comprehensive comparisons provided in visual resources like . A well-informed choice can provide not only financial security but also peace of mind during lifes uncertainties. Moreover, understanding potential pitfalls of various policies can prevent families from making costly mistakes, reinforcing the necessity of financial education—an essential theme in contemporary discussions on insurance, as highlighted by (Baker-Sabino C). As families navigate these decisions, the right policy will serve as a foundational element of their long-term financial planning and stability.